Michael In the USA, the financial activities of every citizen are closely monitored by three private companies: Equifax, Trans Union and Experion. I mentioned this briefly in Rundbrief 05/2001. When you open a bank account, apply for a credit card, or take out a loan for a house -- bam! a notification goes to the three. On the other hand, when you apply for a job with a company or show interest in renting a new apartment -- bam! the company or landlord will ask the three about your financial situation.

Moreover, the three of them learn from every small mistake: If one forgets to transfer the monthly payment to the credit card company just once, it will immediately be prominently displayed in the "Credit Report". If one has 10 credit cards, two leased cars and has financed 3 houses over the last 10 years, like the average American, this report will quickly become confusing.

Since Americans like to keep things simple, financial companies like "Fair Isaac" generate a so-called "Credit Score", a number between 300 and 850 that indicates a person's creditworthiness. The higher the score, the better: 300 indicates a notorious bankrupt, whom nobody would trust. However, from 720 onwards, banks swarm around the customer like moths to a light, this number distinguishes carefully operating people whose transactions have been recorded for some time and have never shown irregularities.

When someone wants to buy a house and applies for a loan, the bank employee goes to the computer, retrieves the score and then offers the customer the interest rate according to an internal table, similar to the following:

| Credit Score | Interest Rate |

|---|---|

| 720-850 | 5.73% |

| 700-719 | 5.83% |

| 675-699 | 6.39% |

| 620-674 | 7.30% |

| 560-619 | 8.66% |

| 500-559 | 9.10% |

It pays off, therefore, to keep one's "Credit Report" in order and to know one's "Score", which could translate into actual money. For Germans who have recently moved to the USA, the Credit Report is simply empty, and it is not so easy to apply for a credit card or to rent an apartment.

The "Credit Report" is kept under the Social Security Number (SSN) of a person. Every American has one. It consists of 9 digits, in the format XXX-XX-XXXX. It accompanies one throughout life, almost everyone knows it by heart. As an immigrant, one is assigned an SSN when registering with the Social Security Administration in the USA with a valid work visa (see Rundbrief 01/1997).

The SSN should be kept secret, because it also serves for identification of a person. For example, when I call my bank, the automated voice asks me for the last four numbers of my SSN before it reads out the account data. When sending an application for a new credit card, the SSN must be on it.

In terms of data protection, one gets the bare horror. Some health insurance companies take the SSN as a membership number and print it on the card so that every doctor's assistant can see it. Every time I write something for an American publisher and get paid for it, I have to submit my SSN so that it is correctly taxed. Recently, a secretary even wanted me to send her the SSN by email - which I had to give a lengthy lecture about how the text of any normal email is accessible to anyone who sits at a computer somewhere between the sender and the receiver. Even the registration form for the Costco shopping paradise asks for the SSN, it's downright crazy!

This total devaluation of the SSN has led to the need to think very carefully about who to actually give one's SSN to. Even if it is asked for, one sometimes has to really say "No!" In recent years, authorities have registered a drastic increase in "Identity Theft" crimes. If someone knows someone else's SSN and also knows their name and address, it is very easy to open accounts, apply for credit cards and do all kinds of mischief. The victims often don't notice this for years until one day the rude awakening comes when unexpectedly high bills arrive and the reputation is ruined. It often takes years for the victims to repair the damage.

Therefore, consumer organizations and the independent magazine "Consumer Reports" (similar to Stiftung Warentest in Germany) recommend that one should check their "Credit Report" at least once a year with the three credit bureaus. This costs $12.95 per bureau (so a total of $38.85) and can be quickly done over the internet with companies like MyFico. There, one not only has to provide their SSN and driver's license number, but also has to answer a series of tricky questions to ensure that they are indeed who they claim to be.

There, you can then see your Credit Score and all accounts, credit cards, and loans you have ever applied for per credit monitoring firm. Additionally, the website shows any irregularities and gives tips on how to increase your Credit Score.

For example, if one has never taken out a loan, one should simply apply for a small one for fun, pay it back properly, and the score will increase. However, if one asks for the credit report too often, this will reduce the score, so be careful!

Since the process works for three companies independently, it is important to check all three to make sure that no mistakes have been made that can be claimed to the respective companies. The companies usually do not delete the mistakes, but comments can be added.

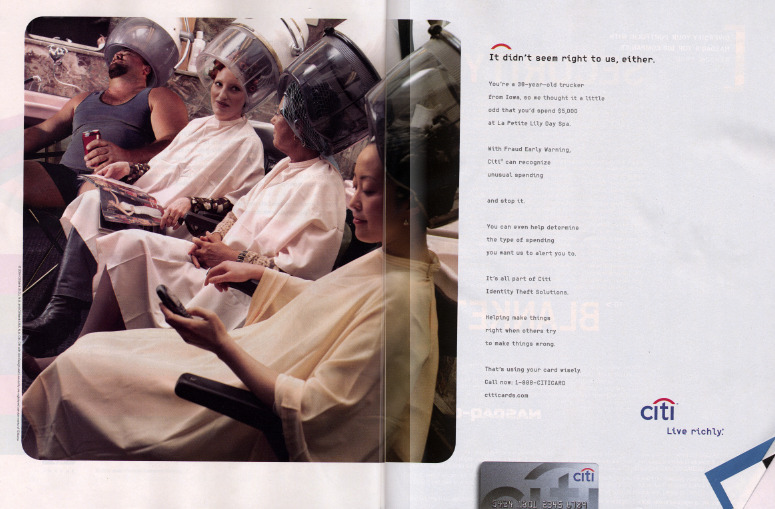

Lately, even credit card companies are advertising that they protect against identity theft by electronically monitoring what people buy and sounding an alarm if the behavior pattern changes abruptly. Newspaper ads like the one in Figure 2 show grotesque situations: a truck driver sitting in his underwear and holding a can of soda in the hairdresser's salon under the dryer. The ad text begins with "It seemed strange to us" and explains that the trucker's credit card was suddenly charged $5000 for a beauty salon and the credit card company stepped in. On television, there are commercials in which a grandmother in a deck chair speaks with the shrill voice of a teenager, telling how she just spent a lot of money on clothes.