Accounts/Checks/ATMs in the USA

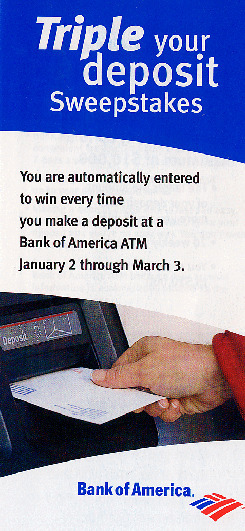

Michael Thank you! Every now and then, something new comes up, and I think to myself: That idea could have been mine. Recently, along with my bank statement, I received a brochure that promised that you could win money by using the bank's ATM. I had this idea back in 1970! But I probably need to elaborate a bit more for the German readers, so I'm making it a main topic in my newsletter: Financial transactions in the USA!

The American word for "Geldautomat" is "ATM," pronounced "Ay-Tee-Em." It stands for "Automatic Teller Machine," which roughly translates to "Automatische Bankkassierermaschine" in German. These machines have three advantages over the German ones, and I don't know if I could live without them: First, you can choose your own PIN instead of being assigned one that no one can remember. Second, there is a button called "Quick Cash." You tell the bank once what amount you usually withdraw from the ATM, and the machine remembers it. Then you just go there, enter your PIN, press "Quick Cash," and the ATM dispenses the same amount of money every time. By the way, ATMs here only dispense twenty dollar bills because no one withdraws huge amounts. Third, and this is what I'm really getting at, you can not only withdraw money from American ATMs but also deposit cash.

Here in the USA, instead of using cash, people often pay with checks. These are so-called "personal checks," which are not like Eurocheques that guarantee the recipient will receive at least 400 marks. Instead, personal checks do not guarantee anything. If someone writes a check and doesn't have enough money in their account, the check "bounces." The word "bounce" means something like "to be rejected." The doorman of a bar or club is called a "bouncer." Or if the train is already full with 24 bicycles and the conductor turns you away, you might tell your fellow cyclists, "I got bounced off the train, man, this sucks big time!" But I digress.

You receive checks from people you know to settle amounts of more than twenty dollars, or, for example, as a payment method for a mail-in rebate -- you know, where you pay more at the register, send in a coupon by mail, and get the money back after a few weeks.

You can then deposit the check at an ATM and the amount is credited to your account immediately. However, you can only access the money once the transaction is finalized and the bank has collected the funds from the check issuer, which can take up to a week. Of course, instead of using the ATM, you can simply go to the teller. In the USA, you typically don't pay any monthly fees for a checking account -- however, at our bank, it costs two dollars each time you have something done by the staff instead of the machine.

Depositing a check at the ATM is quite simple: First, you need to "endorse" the check. You write your name, account number, and signature on the back of the check you received from someone. Then you go to the ATM, take an envelope from a drawer there, put the check inside, and seal it. Next, you insert your ATM card into the machine, enter your PIN, and select the "Deposit" option from the menu. You enter the amount written on the check (if it's an odd amount and you haven't memorized it, you have to quickly tear open the envelope again!) and suddenly the machine starts whirring and opens a flap you've never seen before, eagerly sucking in the envelope you hold out. What happens next, I can only guess: The next day, a bank employee opens the envelope, checks if the amount was correct, and processes the transaction.

Exactly this check depositing (and you can also deposit cash this way) is currently being rewarded by our bank with a chance to win a prize. Every time you deposit a check and luck is on your side, you can win three times the deposited amount. Therefore, if you've ever wanted to send me a check, send it now!

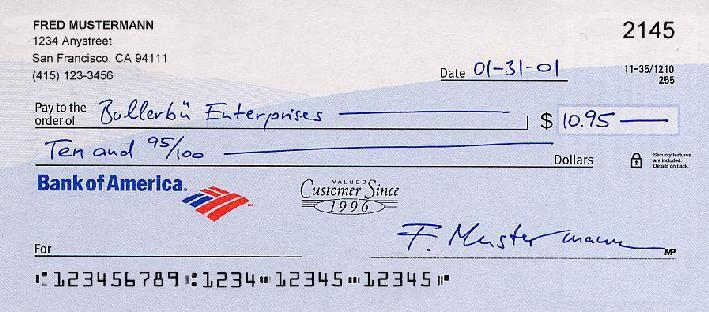

Now the question -- how do I write a check? In Figure 4, you can see an example. Let's assume I received an invoice from a company called "Bullerbü Enterprises" for 10 dollars and 95 cents. I would agree with it and want to send them a check. First, you write the date in the "Date" field at the top right. Month, day, year, separated by slashes or dashes, as is customary in America. In the image, you see January 31, 2001, written as 01-31-01. By the way, in America, you can postdate checks to prevent them from being cashed before the entered date. In Germany, it doesn't matter; the check is always cashed immediately. In America, the bank will not cash it before the entered date.

Then, in the "Pay to the order of" field, you enter the name of the company that will receive the check, in this case, "Bullerbü Enterprises." It is very important to write the name correctly, as the check is only valid for this company or person--for security reasons, since it could get lost in the mail. Similar to an "account payee only" entry on a German check.

The amount goes in the field with the dollar sign in front, and in America, the comma is a period, so it's 10.95 and not 10,95. Don't take this lightly; the comma in America is used to separate thousands, so 1,000 means one thousand, which in Europe would be written as 1.000. And of course, the number one is written without a stroke, but educated newsletter readers have known this for years. The amount is then written out again in the field below, first the whole number value, followed by the word "and" and the cent amount as XX/100. In our case, it's 95 cents, so it reads "Ten and 95/100". Quite unusual, but that's how it's done in America.

As with German checks, you should fill in the blank spaces in the fields with horizontal lines so that no one can tamper with them. Then don't forget to sign, and you're all set. In the "For" field, you can enter a kind of purpose, such as writing the phone number when paying the phone bill, or perhaps the name of the magazine and the subscription duration for a magazine subscription, but this is all optional and will most likely not be noticed by anyone. It's sometimes quite useful just for your own bookkeeping.

In the top right corner of the check, you will find the current check number (2145), and at the bottom in the machine-readable section, there are first 9 and then another 4 digits for the routing information (a type of bank code), followed by two sets of five numbers for the account number (12345-12345 in the illustration).

Then you stick a 34-cent stamp on an envelope (that's how much it costs to send a letter within the USA that weighs no more than one ounce, about 28.35 grams) and send it off. On your invoice copy, you write "Paid 01/31/01 Check #2145" and file it in a folder so you know that you've paid the bill in case a reminder comes at some point, and also with which check. If the check gets lost in the mail, you can call to have it canceled at the bank, so you can send a new one. This happens in about 1% of cases. In your checkbook, you record that a check for the amount of $10.95 was written and calculate how much is left in your account. If you forget to do this, you might end up writing checks that aren't covered, and they "bounce," which is uncool.

By the way, you might be wondering how you can be sure that a check you receive is covered. Because a "Personal Check" does not have guaranteed coverage, hardly anyone accepts one except for the corner supermarket, which will also ask to see your ID. In such places, it might happen that bounced checks are publicly displayed so everyone can see what kind of fool doesn't have enough money in their account. Letting a check bounce is considered pretty foolish, and if it happens to someone once, they are forever discredited.

So, for example, if you're buying a used car, no one will accept a "Personal Check." Once the purchase price is negotiated, the buyer goes to the bank and obtains a so-called "Cashier's Check," which is guaranteed to be honored. By the way, the cashier's check has a detachable side strip. I've heard that if you tear it off, the "Cashier's Check" is no longer valid! The bank requires real cash from the account for a "Cashier's Check," otherwise, they won't issue it. The buyer then takes it to the seller, and the purchase is finalized. Why use a "Cashier's Check" instead of cash? Because of the traceability of the transaction. With cash, no one can prove who received what and when. However, when a check for a certain amount is cashed at a bank, it is officially recorded because the bank logs it.

What if you buy a used car on a Saturday? In the USA, the customer is, of course, not the fool but a king -- and so some banks are naturally open on Saturdays as well. By the way, it's quite funny because that's when they have "Casual Day," meaning none of the employees have to wear a suit with a tie, or a costume. Angelika and I went to our bank four years ago, when we were new in the country, on a Saturday to open an account, and someone in jeans and a shirt approached us in the lobby to ask about our needs. Confused, I thought, "What does the janitor want from me?" but it was a bank employee from the counter who was walking around the customer area! It's funny what you have programmed into your brain.

"Traveller's checks" that can be purchased at banks in Germany are, by the way, the ideal means of payment for tourists. Amex traveller's checks are accepted everywhere here in the USA, as long as they are issued in dollars. Even the corner store or a restaurant will gladly accept them without any fees to settle the bill, as long as you don't try to pay a $5 bill with a $100 traveller's check. Otherwise, tourists are best off using a credit card, as it offers the best exchange rate and only about 1% in fees. With cash, the exchange rate is approximately worse by 5%.

It's also amusing what happens when you first arrive in the country and receive your first checkbook, usually containing about 20 so-called beginner's checks. Absolutely no one accepts these, except for the electricity company and the telephone company, to whom you send a check by mail each month to pay your electricity and phone bills. If you don't run into trouble with the first checks, the bank will send you a proper checkbook after a few weeks. Since many stores are rather dismissive towards people who have just received their first checkbook, the bank will suggest starting the check numbers not at 1, but at, for example, 1000. Over the years, you build up "credit," or creditworthiness.

At some point after a year, you can apply for a credit card. Incidentally, it doesn't matter if you already had a credit card from the same company (American Express, Visa, MasterCard/Eurocard) in Germany; American credit companies don't care about that at all. Most Americans come into contact with credit very early, and similar to the "Schufa" in Germany, the American "Credit Report" records who repaid their debts and who didn't. Three private companies maintain "Credit Reports": TransUnion, Experian, and Equifax. Because these are private companies, you have to be extremely careful to ensure no errors slip in. For example, if a bank reports just for fun that someone hasn't paid their credit, you can file an objection against the entry (which will then be noted in the entry), but the entry itself remains. I've read that people have had to fight against these arbitrary or erroneous entries for years before they were finally corrected. The best stories, by the way, are in the very good book https://www.amazon.de/exec/obidos/ASIN/0596001053/perlmeistercom04 by Simson Garfinkel.

Anyone who once fell out of line (even if it was just for not paying the rent, missing an installment payment, or running out of money in the account) has a very hard time correcting this mistake. When you apply for a credit card, the card company checks the "Credit Report" to see how creditworthy the potential new customer is. In the case of a foreigner newly arrived from Germany, this inquiry results in a blank sheet of paper, which leads to the automatic rejection of the application. The same applies, by the way, when renting an apartment: the landlord checks the "Credit Report," and if there is something negative or nothing at all, you don't get the apartment. At that time, I had to plead with our landlord until I finally got our apartment -- because my credit report was simply empty.

Having "credit" or creditworthiness is very important in America. If someone pays amounts over 20 dollars in cash at the supermarket, they are looked at strangely, as if the cashier is thinking: Why doesn't anyone give them a credit card or a check? What's wrong with them? However, I still like to pay in cash, and I don't care what they think of me. On the contrary, it drives me crazy when some fool pays a 5-dollar purchase with a credit card, and it takes forever--quite common in America. Those with a good credit receive about two offers every day (by mail or phone call) for new credit cards. This starts happening to foreigners who haven't had any negative incidents after about two years, as they become known in the system.

Cash, on the other hand, provides anonymity--no one can trace who bought what, where, and when. However, supermarkets are naturally interested in collecting data on purchasing behavior and selling it back to advertisers, who then bombard you with targeted, tailor-made advertising. For example, a check might have your phone number on it, which the supermarket can sell to people who call you at 8 PM at home trying to sell you something. If the bank doesn't write the phone number on the check, the cashier will ask for it. Of course, you can say you don't want to provide it or just give a fake number like 123-4567, but it's amusing. Supermarkets like "Safeway" issue customer cards, and certain special offers are only available at a discounted price if you present the customer card. And you can't even enter our favorite supermarket, "Costco," without your membership card! This way, the supermarket knows who bought what and has more data to feed into the computer. I don't think this is bad at all because the advertising that bombards us today is so annoying precisely because it is not targeted. When the TV interrupts a program for 5 minutes to show beer or detergent ads, it's a waste of time. If, during the same time, computer stores advertised their products, I might not have any objections.