Angelika Every year in April, millions of American tax payers and consultants get very busy because no matter what, on April 15th, every person subject to income tax has to submit their tax documents for the previous year. Thus, this past April 15th, we submitted our tax declaration for the year 2013. Only if Aprith 15th falls on a weekend or holiday, the deadline gets extended until the next business day. It is possible to delay submitting the tax return by six months by filing for an extension until October 15th. But this doesn't mean you could pay taxes owed at a later date. If tax payers estimate that they owe taxes, they need to prepay the amount by April 15th, regardless of their extension status, or they will get hit by additional interest and penalty fees later. For this reason, I've never really understood why people file for extensions in the first place, because if I have to calculate how much I potentially owe anyway, I can just as well finish up the forms and submit my return, unless I know for sure that I'll always get money back by the Internal Revenue Service (IRS).

Obviously, preparing our income tax forms isn't exactly my favorite activity, but since taxes are somewhat inevitable, I thought it might be of interest to our readers on what exactly a U.S. tax return entails. What's being taxed and what can you deduct? I promise I won't bore you with agonizing details, since a U.S. tax return can be arbitrarily complex, just like the German one. There's a thousand and one exceptions and special cases. Instead, let's focus on form 1040, which is the form every U.S. income taxpayer has to deal with in some form or another. About 70% of all taxpayers use this form, and depending on how complex their tax situation is, there's a number of additionally required forms, called schedules, each of which is marked either by a single letter or a four-digit number. Here are some of the widely used schedules, to be submitted along with the main form 1040:

Schedule A: This is the form for claiming itemized deductions: 1) Medical expenses covered out of pocket. But they must exceed 10% of the taxable income. 2) Taxes paid in the state of residence over the last year. This might sound strange to you, but in fact, it makes a lot of sense, since some U.S. states don't have an additional state income tax at all (Alaska, Florida, Nevada, South Dakota, Texas, Washington, Wyoming), while states like California or New York ask the taxpayer for significant amounts of extra money. In these states, taxpayers submit two different income tax return, a federal one and another one for the particular state of residence during the tax year. It's crazy, I'm telling you. After having completed the federal 1040 form and a dozen other schedules via the tax software program "Turbo Tax", the odyssee continues with with the California tax return, only that the form is called 540 there, welcome to insanity! 3) Interest payments for home mortgages (within limits). For example, if a married couple is paying $12,000 in interest for a mortage on their house, they can deduct about $4,200 from their income taxes. 4) Donations to charity, up to 30%-50% of the taxable income 5) Losses caused by theft or accidents (for example natural disasters), but only if the amount exceeds 10% of the taxable income. 6) Other expenses like job-related charges not reimbursed by the employer, or what the taxpayer had to spend for tax consultants or tax software, but only if they exceed 2% of the taxable income.

Schedule B: If you've had more than $1,500 last year in income from interest and dividends, you need to submit the Schedule B form. The first part lists the interest income, the second the dividends from stocks. This doesn't mean that interest below $1,500 isn't taxed, every single cent in interest and dividends needs to be taxed, it's just that for less than $1,500 there's no requirement to fill out the form, because you can list this capital income on the main 1040 form. If the tax payer owns foreign accounts, there's a section in part 3 of Schedule B which requires to name them, and to state in which country they're located.

Schedule C: Self-employed taxpayers use this form to calculate their financial gains or losses from self-employed work and the required tax payments.

Schedule D: This is where you list gains and losses from selling stocks and mutual funds. There's a difference between short term gains of stocks held for less than a year and long term gains if you've owned a stock for more than one year. The tax rate is different in each case, on short term gains, it is equal to the tax payer's income tax rate, and for long term gains, it's between 15% and 20%. You can claim a consolation prize on realized losses by balancing them against gains, and only pay tax on net gains. But there's an exception, the so-called "wash sale" (Rundbrief 05/2010). If someone has had a particularily bad year and had more losses than gains, they can deduct up to $3,000 of those losses from regular income. If they've lost more than $3,000 in a year in the stock market, only $3,000 can be deducted in this way from regular income in the current year, but the remaining loss can be rolled over to following years.

Schedule SE (Self-employment Tax): Self-employed individuals use this form to calculate what they need to pay for Social Security (federal low-level retirement income) and medicare (federal health insurance for retirees).

I've mentioned here a while back that there's no need to submit any invoices or receipts with the tax return (Rundbrief 05/1998). Every U.S. bank or brokerage house will send detailed information on how much interest or dividend income was generated during the year, or which stocks were sold to the IRS on behalf of the account holder. Copies of these 1099 forms are also sent to the taxpayer each year at the end of January. The taxpayers also receive three copies of the "W-2" form from their employers, it lists the yearly income, and how much was already deducted from it in social security and income taxes. When submitting the tax return, the tax payer staples the "W-2" form to the return, unless it's transmitted electronically (called "e-filing"), in which case it's no longer necessary.

The IRS identifies taxpayers by their social security number (SSN), which every U.S. citizen automatically obtains at birth. Immigrants in some visa categories won't receive an SSN, and, quite interestingly, there's millions of illegal immigrants living in the U.S. without one. When these residents set out to dutifully pay their taxes, the IRS is looking the other way, as it wants tax income, and isn't interested in people's immigration status. In these cases, law-abiding taxpayers receive a "tax identification number" in lieu of the SSN. Either number goes on every tax form, including the aforementioned 1099, where it serves to identify individual taxpayers.

Before you start filling in tax forms, it is advisable to determine your tax category, called "filing status". In total, there's five different classes: 1) "Single" 2) "Married, filing jointly": if a married couple returns a single, combined tax return, regardless if both or only one spouse is working 3) "Married, filing separately": when two spouses file separate tax returns, which can be beneficial if their income is about the same 4) "Head of Household": for example if a single parent raises a child 5) "Widow/Widower with dependent child": this status may be selected after up to two years after one spouse has died. In general, depending on the filing status, the tax law offers different tax exemptions and varying amounts.

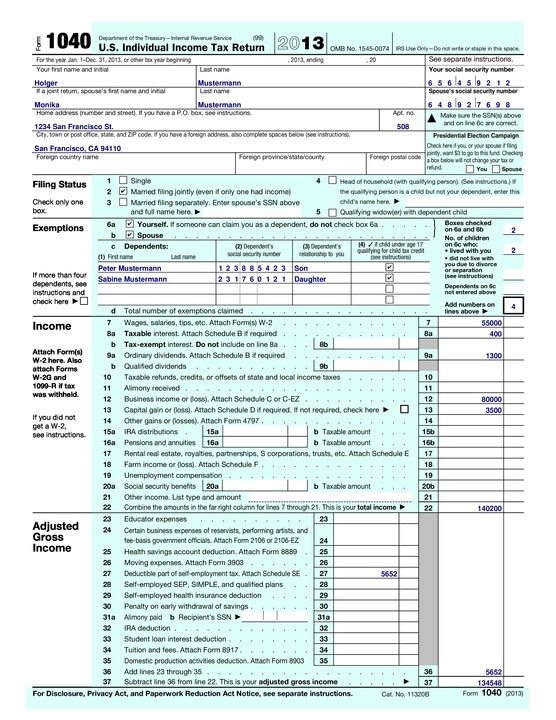

To make this more accessible, let's go through a specific example. Holger and Monika Mustermann are two Germans holding U.S. Greencards and are living in San Francisco with their two school-aged children. They've been residing in the U.S. for five years now, and for the entire year of 2013, they've been living and working in San Francisco. This is why they are paying taxes on their worldwide income to the U.S. Internal Revenue Service. The married couple submits a joint return ("Married, filing jointly"). Monika works as a teacher at a public school in San Francisco and gets $55,000 a year. Holger is a self-employed author and made $80,000 in 2013. On the submitted 1040 form, Monika writes down her salary in line 7 and Holger's net income from self-employed work goes on line 12.

Holger calculates his gains from self-employed work by completing schedule C. Aside from that, the couple received $400 in interest savings accounts, $200 of which originated from a German bank account. They also received dividend payments of $1,300. All of their capital gains are listed as regular dividends on the 1099 form, and they're taxed at the the couple's income tax rate. In comparison, dividends categorized as "qualified" are only taxed with a lower rate between 15% and 20%, which applies to virtually all dividends paid by U.S. companies.

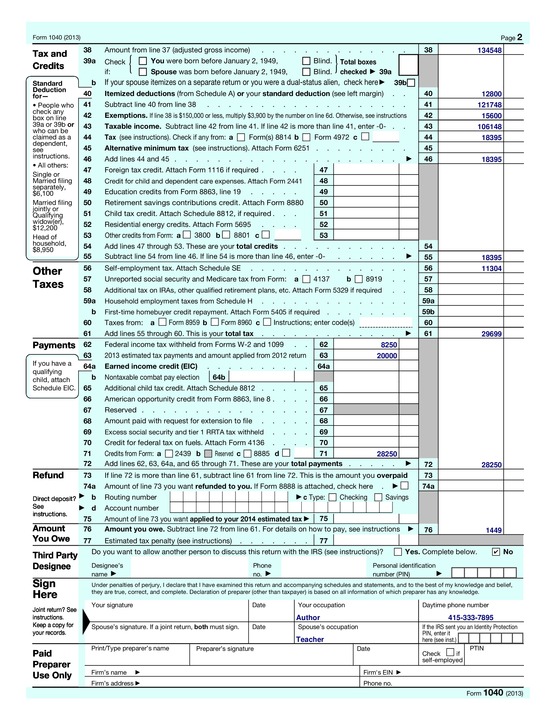

Although Holger and Monika have earned less than $1,500 in interest, they need to complete schedule B, since they own a foreign bank account in Germany. Holger also sold some Amazon stocks and gained $3,500, as he calculated in schedule D and then entered in line 13 of the 1040 form. The total income for the year 2013 in this example is therefore $140,200, as you can verify by adding the amounts $55,000 + $400 + $1,300 + $80,000 + $3,500. Since Holger is self-employed, he can deduct 50% of the social security payments he made, which lessens the total income by $5,652, which is now down to $134,548. This amount is called "adjusted gross income". Now it's time to deduct qualified expenses to reduce the taxable income even further. First off, the Mustermann family has deductible expenses of $12,800, as calculated in schedule A. The standard deduction for married couples is $12,200, which is $600 less than what the Mustermann family can deduct, so it makes sense for them to itemize their deductions explicitly in schedule A instead of taking the standard deduction.

The Mustermann family can further claim so-called "exemptions" for every family member living in their household. For the four of them, that's $3,900 per person. Although the family has to pay for childcare, since both parents are working, they won't receive the so-called "child care credit", because their combined income exceeds the limit. In line 57, Holger enters the amount of social security contributions he had to pay because he's self-employed. Holger also pre-paid $20,000 in estimated taxes and Monika's employer already withheld $8,250 in federal income tax contributions. All of the above considered, the family now owes $1,499 in federal income taxes. If they send in the income tax return by mail, they simply include a check for the amount of $1,499. If they opt for e-filing, they can conveniently pay the amount they owe by credit card.