Angelika The persistent view holds that every American pays even the smallest amounts with their credit cards, and when paying with cash, people roll their eyes in a condescending way: "Look at this poor guy, he has to hand over bills because he can't get a credit card." However, it's not quite that bad. You pay for your coffee at the "coffeeshop" in cash, and no one finds it strange. On the contrary, many smaller businesses even set a minimum amount (between 5 and 15 dollars) from which customers can pay with credit cards.

On the other hand, it is true that American daily life is difficult to manage without a credit card. Try booking a car, hotel, or flight without a credit card; it's a hopeless endeavor. When I first traveled to the USA at the tender age of 21, I didn't have a credit card because German banks at the time wouldn't dream of issuing one to a penniless student. My friend Marianne and I wanted to rent a car in Las Vegas without a credit card and had to sift through the Yellow Pages of Las Vegas until "Brooks-Rent-A-Car" finally agreed to give us a car if we deposited our return flight tickets and some travelers checks. Or take shopping online: since America doesn't have the direct debit system as understood in Germany, nothing works without plastic money.

In America, credit cards actually embody what the name promises. When a customer pays with a credit card, credit is granted, and interest accrues after a certain period, the so-called "grace period" (usually 20 to 25 days). In Germany, at least in our time, it was still common to link the credit card to the checking account, meaning the amount due was simply debited from the account (let us know if this has changed in the meantime). Such cards do exist in America as well, but they are called "debit cards" and are not considered real credit cards. However, they are indispensable for foreigners who have just settled in the USA and have not yet obtained a traditional credit card.

As long as the credit card holder keeps paying their credit card bill, which arrives once a month, on time and in full, they are in the clear. But beware, if interest and fees accrue, then paying with a credit card is actually the dumbest thing you can do, because credit card companies really take advantage. The level of interest and fees and the methods used are comparable to loan sharks; there was an interesting article about it recently in "Consumer Reports" (similar to the German "Stiftung Warentest").

First, there are different interest rates depending on what the credit card holder does with their credit card. If they withdraw cash from an ATM with their credit card, a different, higher interest rate applies than if they use it for purchases. Additionally, the "grace period" is eliminated for cash withdrawals, even if you always pay your bill in full, meaning interest accrues as soon as the ATM dispenses the money. Furthermore, customers are usually charged a fee of 2-3% for using the ATM. The credit card company lists on the bill which interest rate applies in which case. For example, with our Chase Visa card, it's 22.74% for cash advances and 18.74% for other purchases. (By the way, we pay our credit card bills in full every month).

Behind the percentage listed lies the annual percentage rate (APR), which varies from customer to customer. The free market rules here, as there is no law that dictates how high this interest rate can be. If you pay your bills late or exceed your credit limit, there are not only penalty fees, but the annual interest rate is also adjusted upwards. So don't believe the TV shows where the waiter politely and discreetly returns the credit card because it has been maxed out and the transaction couldn't be processed. In real life, the credit card company would rather charge the customer an average of 30 dollars for this offense and allow further charges on the card.

The credit limit granted is determined individually for the customer by the credit card company. If we use certain cards frequently, our credit limit miraculously increases after some time. Many credit card companies even increase the annual percentage rate if the customer pays a bill from another credit card late or applies for a new credit card, citing that the customer's behavior poses an increased risk for them as well. The customer might be in financial trouble and need a new credit card for that reason. The companies obtain information about the individual customer's payment behavior by accessing the much-discussed "Credit Report" (Rundbrief 05/2004) With our Chase card, paying the required minimum payment late could cost us up to 39 dollars. The minimum payment is the portion of the granted credit that must be paid off each month, no matter what, usually 2% of the outstanding balance, which is not exactly a huge amount. Many financial advisors and consumer associations bitterly complain about this because if you only pay the minimum required amount and nothing more, it can take years to pay off the Christmas gifts that were all bought with a credit card.

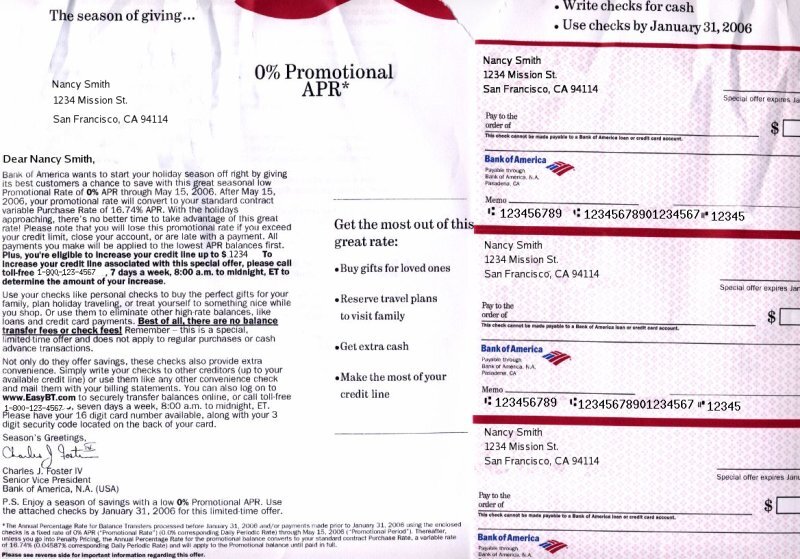

Many credit card companies also try to attract new customers by offering them favorable introductory interest rates (or even interest-free periods) for a few months. They are particularly interested in having you transfer balances from competitors' cards to the new card. We constantly receive such offers: "0% Introductory Rate." This initially sounds good to many, but the interest rate naturally increases after the introductory months. And often, the favorable rate only applies to the transferred amount and not to any new purchases.

Although everyone thinks that there are countless companies offering credit cards, the five largest, namely JPMorgan Chase, American Express, MBNA, Bank of America, and Citigroup, dominate 65% of the market, according to the Consumer Reports magazine in November 2005. Of course, credit cards still come in a variety of different designs. Michael particularly loves the cards that have some kind of bonus programs, such as getting 2% cash back on certain purchases at the end of the year or being able to collect eBay points when using the card. However, we always attract the most attention with our Linux Mastercard (incidentally from MBNA), which features the Linux penguin on the card. Everyone always comments on how nice it looks, but they usually don't know that behind Linux lies Michael's favorite operating system for the computer.